10 Trends That Will Change Real Estate in 2022

While the housing market is still hot, could there be signs of a cooldown ahead? How will technology affect real estate in 2022? What’s the forecast for real estate teams and new construction? And who exactly is tomorrow’s buyer?

Leading Brokers & Coaches Share Insights on 10 Trends that will Influence Real Estate in 2022

Earlier this year a Zillow research study reported that almost 70% of real estate experts surveyed said they expected more houses to list in the second half of 2021 or the first half of 2022.

Of course, more inventory typically means a drop in values; yet, with buyer interest still high and mortgage rates still hovering at historically low levels, the post-pandemic tailwinds continue to sail.

Meanwhile, rents are rising, supply issues are stalling new construction starts and artificial intelligence is poised to rapidly evolve the way agents will search clients and properties.

To get a handle on what’s around the corner in the coming year, we consulted leading brokers and real estate coaches to share their insights on the top 10 trends that will influence real estate in 2022.

Trend #1: Values Continue to Rise — Albeit Not at 2020 Warp Speed

Heading into 2021, the U.S. median home price centered at $340,000 with inventory nearly 40% below December 2019 levels — making 2020 the lowest housing inventory year in recorded history.

Now that eviction moratoriums are lifting and more sellers are listing, inventory is certain to shift. Still, the question remains: Will real estate values continue to climb on an upward trajectory?

Most experts concur that prices will grow due to continued high buyer interest, though just how much growth the market will sustain remains to be seen.

“I don’t think we’re anywhere near the end of appreciation trends,” says Joseph W. Rand, Chief Creative Officer for Howard Hanna | Rand Realty. “In most parts of the country, we’re still at or below the inflation-adjusted average sales price of the last seller’s market. If rates stay low, and the economy continues to improve, buyers have the ability to stretch to meet those higher prices.”

On the other hand, Chris Suarez, co-founder of PLACE sees the amount of appreciation slowing. “This is due, not solely because the market is done absorbing the pent-up demand that came from the pandemic, but also from the looming inflation and global uncertainty related to security that has historically slowed home sales. At this point, it does not look like a huge ‘full stop’ but more like a gradual slowing, which customarily follows a fast market.”

While original forecasts in December 2020 predicted housing prices would climb 8% in 2021 and 5.5% in 2022, home prices have already seen a 23% increase in 2021 — almost triple those original estimates.

Moving into 2022, the CoreLogic HPI Forecast predicts home prices increasing on a year-over-year (YoY) basis by only 2.2% from August 2021 to August 2022; while, Freddie Mac projects 5.3% for the new year.

Home sales, meanwhile, are ending the year on a high note. According to a recent report from Zillow, pending home sales and purchase loan applications have been stronger than expected with more than 6 million sales of existing homes to close in 2021 — 7% more than 2020 and higher than the company’s former projection of 5.9 million sales.

Trend #2: Post-Pandemic Real Estate Tech Adoption

Clearly, the pandemic served as a catalyst for agents and brokers to adopt new forms of digital technology as a means of minimizing in-person contact.

From drone videography and 3D tours to virtual reality and even augmented reality, real estate clients now have a variety of digital imagery to view a home.

But the real disruption in real estate goes well beyond drones and videos. Today’s tech allows agents to create offers on a phone in 10 minutes or less; request digital earnest money deposits from clients; and set up online notarizations of documents.

Real estate agents can integrate all of their real estate software, from CRMs, accounting and marketing platforms with an open platform transaction management system that improves the client experience while providing visibility into closed lead sources. In fact, the entire home buying and selling experience can be handled virtually electronically.

As Chris Stuart, President of PLACE notes, “I still can’t believe how many top producers are settling for mediocre integrations across all aspects of their business. Identifying, integrating and scaling key operating systems will be ‘table stakes’ in the very near future for top producers.”

Indeed, real estate technology is just beginning to awaken. As Rand notes, “We haven’t even scratched the surface of how increased technological comfort levels and competence for both consumers and agents could change the process of buying and selling a home.”

Trend #3: Artificial Intelligence & Machine Learning Get Smarter

In the future, artificial intelligence (AI), and machine learning (ML) will further infiltrate mobile and desktop technology by helping CRMs and aggregate search sites to evaluate properties, predict commissions of impending closings and recognize trends.

At Inman Connect Now, Steve Gaenzler of Red Bell Real Estate, LLC, explained how AI can be used to discern the finer details of a listing’s picture through the use of advanced computer vision. In what might take an agent hours to perform, image recognition — a form of computer vision — can evaluate all the pixels in an MLS picture, satellite or video imagery in a fraction of the time to reveal a set of like properties.

Think of autonomous vehicles, which are already using image recognition by recognizing surrounding vehicles and converting those images into actionable insights. For real estate, image recognition will empower agents to quickly identify and narrow down searches to find those distinctive, subjective details that aren’t necessarily captured in the listing information, such as desired layouts, floor and wall finishes, view type, landscaping and room conditions.

“What makes two otherwise identical houses next door to each other sell for different prices?” asks Dan Foody, Co-founder and CEO of Cloze. “The text of the listing will never tell you, but the photos can. The next big advancement in pricing will be deep learning AI that looks at interior and exterior photos and videos to suss out the intangibles that make one home more desirable than the next.”

Matt Vigh,co-owner of Prospect Boomerang, a Tampa, FL-based real estate recruiting company focused on coaching brokers, also sees AI, ML and big data becoming more relevant in real estate. “The biggest and most obvious place I see it factoring in is making CRM followup exponentially more effective. It will learn to better aggregate what is clicked, opened, forwarded, liked and so many other data points that the CRM will not only listen better, but it will gather and share valuable content more timely than an agent can.”

Trend #4: Mobile-First is the Future

Already, mobile-first platforms are favored by real estate professionals for their portability and ability to get transactions completed on the go. In the future, however, agents will rely even more heavily on their mobile-first apps, allowing everything carried out on a desktop to be done on a smartphone.

Armed with faster browsing and download speeds, more real estate agents and clients will turn to their handhelds to view 3D videos, vet lenders, scan docs and complete the real estate transaction. And as more devices become connected to the Internet of Things (IoT), real estate agents will increasingly use their devices to perform functions, such as turning on the lights of a home remotely.

Not only will a robust mobile device help move the transaction forward for agents, admins and transaction coordinators; it will also become an absolute necessity to connect with tomorrow’s millennial buyer, who’s already using their phone to view listings, research comps and find an agent.

As PLACE’s Stuart notes, “If you’re not currently delivering or working toward a delightful consumer experience in all aspects of the real estate transaction and core service experiences on a mobile device, you’re going to get left behind.”

Trend #5: Teams Continue to Surge

In 2020, the top 1000 teams’ sides increased by nearly 50% YoY, with the average team doing approximately 253 closed sides. Team sales volume also increased by nearly 50%, according to RealTrend’s Thousand List.

But they’re not done yet. In 2018, when NAR conducted its last Teams Survey, 26% respondents claimed to be members of a real estate team. Moving into the future, teams are expected to play an even more dominant role in the industry’s growth.

So why are teams all the rage? First, they’re able to stay agile in a demanding market by providing next-level specialization. Agents like the learning opportunities teams offer and the ability to share workloads. Clients like their fast responsiveness.

Second, many agents favor the ability to start their own team and remain affiliated with a regional or national brand without having to absorb the costs, workload and liability of opening a new brokerage, says Jim D’Amico, CEO/President, Century 21 North East and Century 21 Integra, based in Danvers, MA, and St. Petersburg, FL.

According to D’Amico, teams allow agents with superior leadership skills to expand their transactions by leveraging “people power” to manage tasks, surplus clients, marketing and community involvement, often while still selling homes at a high level.

PLACE’s Suarez sees the real story as the focus on the end user, the consumer. “The consumer is making a clear distinction and decision that they want to work with people who specialize in their field,” Suarez says. “Teams have skilled up, provided better service, embraced technology and moved toward specialization. Teams can deliver a better experience to the consumer, which is what the consumer demands.”

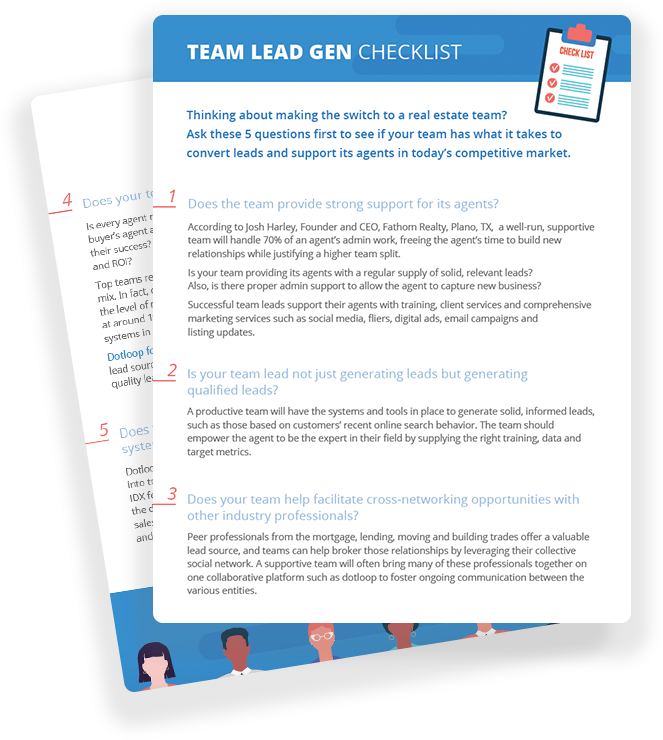

FREE: Team Lead Gen Checklist for a Competitive Market

Ask yourself these 5 questions to see if your team has what it takes to thrive in a low-inventory housing market.

Trend #6: Work From Home Here to Stay

An overwhelming majority (95%) of more than 100 economists and real estate experts surveyed by Zillow view an increased preference to work remotely at least part-time as here to stay.

Studies have found productivity remained at least on par for company employees working from home during the pandemic compared to previous years working in-office.

While Suarez sees the pandemic “as a unique moment in history — a cycle in which people will return to the office,” Vigh sees the trend only proliferating further affordable, outlying suburban and rural growth. “In other words, as long as I can get WiFi, I’m fine!”

People who had previous designs on moving out of the city precipitated most of the pandemic’s “urban-to-suburban exodus,” Rand notes.

“That migratory surge has mostly played out,” he says. “But for the longer term, the work-from-home trend is going to help expand the viable suburban market. People who only have to commute one or two days are more willing to add a half hour to their commute to get more house for their money.”

Trend #7: 72 Million Millennials Dominate Buyers

Expected to comprise over half of the market in 2022, millennials — all 72 million of them — are ready to buy their first home with an average household income of $88,200.

Bypassing the boomers who took over the home buying scene in the Seventies and Eighties, these late twenty-, early thirty-somethings search homes on their mobile devices and follow online reviews and referrals.

“People can wind themselves into knots trying to figure out ‘what millennials want,’ Rand says. “It’s pretty straightforward. They want an easier, cleaner transaction. More digital. Less analog.”

Texting is generally the millennial’s language of choice for asking questions and booking appointments, but they’ll pick up the phone for urgent matters.

While many expect a huge surge of millennials to hit the buyer’s market, Vigh notes, “Millennials put more emphasis on their personal passion for living than on the desire for a more traditional lifestyle,” he says. “It’s ‘Can I see myself living here while I get my food truck business up and running?’ versus ‘Here is where my family will grow up and I will retire.’”

Still, 72 million millennials adds up to a huge buying population and a prime economic force ready to do business in 2022.

Trend #8: New Starts in New Construction May Stall

Consider in 2020 there were 1.38 million housing starts, and the new crop of houses expected to break ground by the end of 2021 may reach 1.56 million.

But the past two years combined have witnessed supply issues and skyrocketing prices for steel, lumber and concrete, as well as new home goods such as heating units and windows.

According to the National Association of Home Builders (NAHB), lumber prices alone rose by as much as 250% since 2020 and have added approximately $36,000 to new home prices.

As a result, mortgage applications for new home purchases decreased 16.2% compared from a year prior, according to the Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for September 2021. And, according to the latest Census Bureau statistics, housing starts fell below expectations to 1.6% in September.

Trend #9: Rents on the Rise

If pandemic-driven home sales led real estate news in 2020, 2021’s headline will be all about how the sales market triggered an uptick in rent prices.

Since January 2021, the national median rent has increased by a stunning 16.4% — particularly notable considering rent growth from January to September in the pre-pandemic years 2017-2019 averaged just 3.4%.

According to Zumper, the national index for one bedrooms reached a new all-time high in every month of 2021 except for one, and two bedrooms broke the record every month since February.

While rents in 2020 remained largely static, rising home prices, investor interest and a growing build-to-rent market set prices soaring in 2021.

In many big cities, like Miami, Boston and New York City, where rents dropped dramatically in 2020, they’re now bouncing back, in some cases, to where they were in pre-pandemic times.

For real estate agents, the rise in rents might offer new opportunities for converting investors into clients and renters into buyers.

Trend #10: Transaction Coordinators on the Rise

Of all the roles in real estate, that of transaction coordinator has arguably changed the most over the past two years. With teams and brokerages growing by both transaction sides and volume and remote work carving out a new niche in the real estate industry, more virtual transaction coordinator agencies are taking services online for a per-transaction fee.

Experienced transaction coordinators are in high demand. In 2018, Zippia, a job search site that posts proprietary data and job-based metrics, forecast the role of all transaction coordinators across industries to grow 5% between 2018 and 2028.

But that number may be well under-represented, given the current market and uptick in remote work. Over the last two years, more smaller businesses are getting into the transaction coordinator game, hiring independents at an average rate of $300-$500 per transaction.

Alex Marsolais, owner of Home Free TC (formerly Minnesota Transaction Coordinators) says the Facebook Group she helps moderate, TCs Empowering TCs, was about 1,000 members about four years ago and has since grown to 4,800 members, including independents, in-house executive assistants and some inactives. While she knew of only four other transaction coordinators when she founded her business in 2015. today she says there are at least 10 other transaction coordinator businesses.

Typically, agents who close 10 or more homes a year are hiring transaction coordinators to take care of tasks, such as opening escrow, coordinating inspections and repair negotiations, client communication and managing documents. As a result, the TC role can free up an extra 15 hours per transaction, giving agents’ time back to spend building relationships and showing homes.

As transactions increasingly go digital, independent transaction coordinators will continue to deliver greater value to agents, teams and brokerages. Many come fully trained on multiple systems and because they work as a collective team, agents don’t need to scramble for a replacement if the transaction coordinator should get sick or take vacation. Hiring independent transaction coordinators also cuts down on overhead costs, medical and 401(k) benefits while representing a tax writeoff for the real estate business.

In addition to independent transaction coordinator outsourcing, larger franchises are hiring more in-house transaction coordinators to free up their agents’ time. Keller Williams, for instance, is hiring their own in-house transaction coordinators, and eXp is developing its own in-house transaction coordinator role with many coaches incorporating this into the agent strategy.

In 2022, change may be the one constant in real estate. Stay tuned for more breaking trends as we head into the new year.